… 미국 FOMC 금리인상, 환율 휘청', '.https://nimage.g-enews.com/phpwas/restmb_allidxmake.php?idx=5&simg=2017061508112909277906806b77b12114162187.jpg');)

… 미국 FOMC 금리인상, 환율 휘청', '.https://nimage.g-enews.com/phpwas/restmb_allidxmake.php?idx=5&simg=2017061508112909277906806b77b12114162187.jpg');)

이미지 확대보기

이미지 확대보기

15일 뉴욕 상업거래소 NYMEX에 따르면 미국의 주종 원유인 서부텍사스산 원유 WTI의 7월 인도분 선물시세는 배럴당 44.73달러로 장을 마감했다.

전일 대비 1.73달러, 비율로는 3.7% 하락한 것이다.

종가 기준으로 7개월 만에 가장 낮은 수준이다.

미국 연준 FOMC의 기준 금리인상과 미국 에너지정보청인 EIA의 향후 전망이 국제유가 하락에 가장 큰 영향을 준 것으로 보인다.

IEA는 이날 국제유가 전망 보고서를 발표했다.

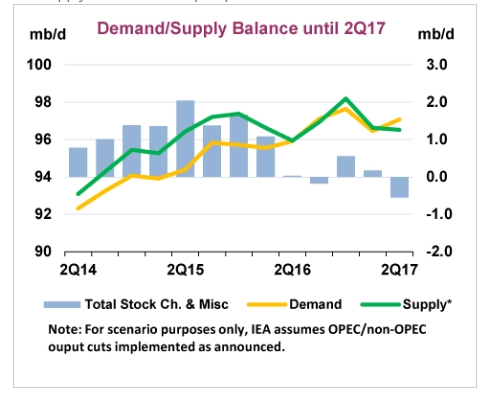

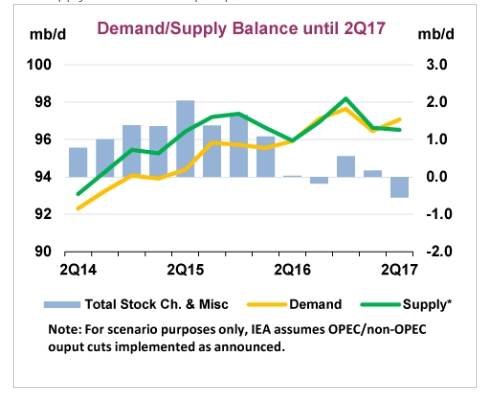

IEA는 이 보고서에서 OPEC의 감산에 무관하게 원유 공급과잉 현상이 지속될 것으로 내다봤다(별표 참조)

다음은 IEA의 국제유가 보고서 전문 요약

In this Report, we publish our first look at what 2018 might have in store. This is timely in view of the recent extension until March of the output cuts. However, such is the volatile nature of the market today, with recent tensions in the Gulf adding to the mix, 2018 seems a long way away. Immediate concerns about stubbornly high stocks due to rising global production are pressuring oil prices, which have fallen to levels not seen since the OPEC ministerial meeting at the end of November.

In April, total OECD stocks increased by more than the seasonal norm. For the year-to-date, they have actually grown by 360 kb/d. Our provisional monthly data for May suggests that OECD stocks might, overall, be little changed, but recent US weekly data suggests that rising domestic production, high imports, low exports, and weaker gasoline demand, have combined to send stocks there higher. In last month's Report, the implied market deficit in 2Q17 was 0.7 mb/d but now this has narrowed to 0.5 mb/d. The reasons for this are a reduction in demand growth, mainly because of weaker Chinese and European data, and an increase in global supply. Based on our current numbers, assuming stable OPEC production, market deficits should be significant in 2H17, although adverse changes to demand and supply data can erode prospective stock draws.

In the meantime, as always these days, the focus is on US production, which, as anticipated in our earlier forecasts, is rising strongly. For 2017, we expect US crude supply to grow by 430 kb/d and the year will end with production there 920 kb/d higher than at the end of 2016. Our first look at 2018 suggests that US crude production will grow year-on-year by 780 kb/d, but such is the dynamism of this extraordinary, very diverse industry it is possible that growth will be faster. For total non-OPEC production, we expect production to grow by 0.7 mb/d this year but our first outlook for 2018 makes sobering reading for those producers looking to restrain supply. In 2018, we expect non-OPEC production to grow by 1.5 mb/d, which is slightly more than the expected increase in global demand.

Back to today; while OPEC countries collectively have broadly implemented their cuts, some members have been less than wholly diligent. Iraq has achieved a compliance rate of only 55% so far this year, and Venezuela and the UAE are also laggards. Meanwhile, two OPEC members not included in the deal have recently seen increases in production: Libya's output has reached nearly 800 kb/d, a level not seen since 2014, and Nigeria has announced the lifting of force majeure for Forcados exports, potentially making available to the market more than 200 kb/d. By the nature of these two countries, production could easily fall back; indeed, in Nigeria the very recent announcement of force majeure for Bonny Light liftings is an example. However, if Libya and Nigeria continue to grow their output these extra barrels dilute the value of OPEC's output accord and contribute to delaying the re-balancing of the market.

The currency used to express re-balancing is the five-year average level of oil stocks. In this report, we show that OECD stocks are currently 292 mb above this level. Indeed, based on our current outlook for 2017 and 2018, incorporating the scenario that OPEC countries continue to comply with their output agreement, stocks might not fall to the desired level until close to the expiry of the agreement in March 2018. A lot can change of course, but, as we said at the start, 2018 seems a very long way away.

We have regularly counselled that patience is required on the part of those looking for the re-balancing of the oil market, and new data leads us to repeat the message in this Report. "Whatever it takes" might be the mantra, but the current form of "whatever" is not having as quick an impact as expected.

김대호 기자 yoonsk828@g-enews.com

![[뉴욕증시] 美·EU 무역협상 난항에 혼조세](https://nimage.g-enews.com/phpwas/restmb_setimgmake.php?w=270&h=173&m=1&simg=2025071905245702748be84d87674118221120199.jpg)